Banking on change – how financial services companies are remaining relevant in the age of digital disruption

![]() Microsoft News Center

Microsoft News Center

The day was 3rd February 1866. Two members of the James-Younger gang entered the Clay County Savings Association in Liberty, Missouri, drew their pistols, and told the teller to hand over the money. The bank’s employees were taken completely by surprise and were, understandably, unprepared for the threat. Up until this point in history, bank heists on the western frontier were extremely rare.

Over the decades that followed, the introduction of state-of-the-art physical and digital security has drastically reduced these types of concerns. However, banks today are navigating a new kind of uncertainty and competitive disruption. Technology is making banking smarter, faster and more intuitive than ever – so much so that Gartner estimates 80 percent of traditional financial firms will go out of business by 2030.

For banks across the region, the stakes are high. The incredible rate of smartphone penetration, combined with a burgeoning youth population, is giving rise to rapid innovation in the financial services industry. According to research conducted by Tenemos and The Economist, banks in the Middle East and Africa (MEA) are recognising the need to evolve, with more than half aiming to become “digital ecosystems”.

On the transformation journey

This early recognition of the benefits of digitisation has meant the financial services industry (FSI) in MEA has been quick to adopt newer technologies and is currently a front-runner in the use of artificial intelligence (AI). Recent Microsoft-EY research found that 38 percent of FSI companies in MEA are already putting AI to active use across their daily operations – more than any other industry, which are still largely in the piloting phase.

Banks are embracing AI predominantly to detect fraud – the modern-day James-Younger gang – as well as to better understand and deliver personalised services to customers, and meet regulatory obligations by streamlining compliance efforts.

Data at the core of transformation

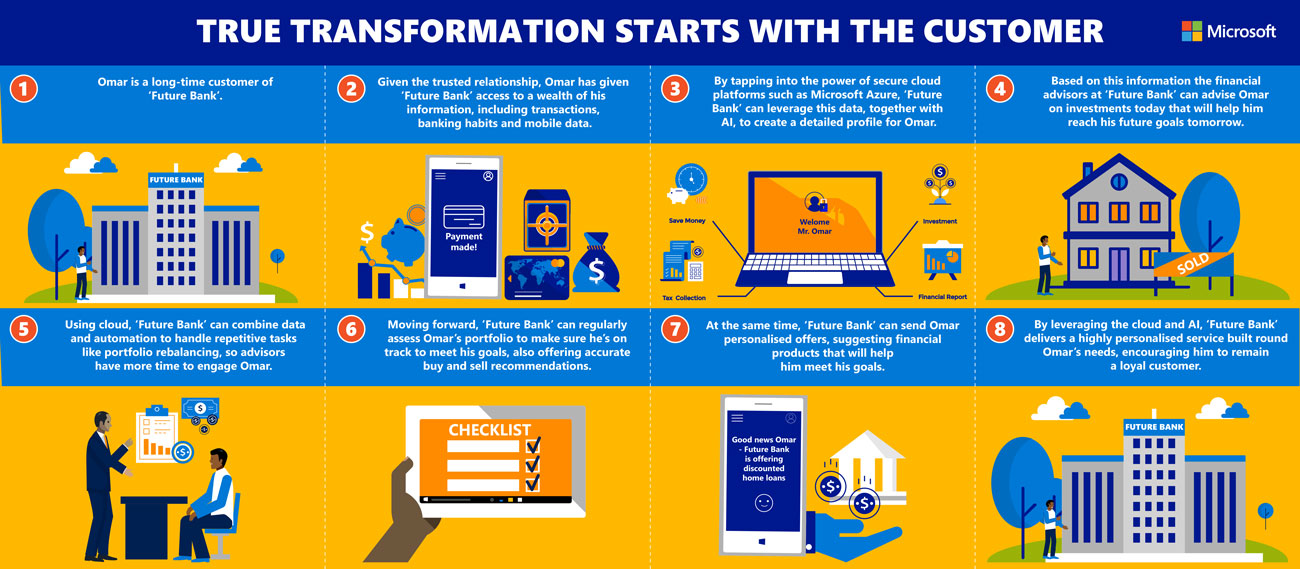

Banks are also fortunate to already have rich pools of quality customer data, which has given them the early foundation needed to build digital ecosystems. What banks are doing now is integrating legacy IT systems with powerful cloud computing to derive intelligent and actionable insights from this data. These insights are helping banks place customers at the very centre of their strategy, and give them a far more compelling proposition. Consider the following scenario:

A future-proof value proposition

This level of customer-centricity is key for businesses across the full spectrum of the banking industry, from more consumer-focused retail banking to commercial banking. Forward thinking businesses like UAE-based Anglo-Gulf Trade Bank (AGTB) are starting their journey by anticipating what the client needs.

As the world’s first fully digital trade bank, AGTB’s market proposition is based on simplifying and supplying client-centric trade banking. Having assessed the most common ways banks service their clients, it knew the manual approach of sending and uploading files, dealing with scans and excessive paperwork had to change.

AGTB set out to fully automate their solution, enabled by new tools like data analytics and rule-based algorithms to help better understand data. One specific solution the company looked at was enterprise resource planning integration and how connectivity could be used to manage the information exchange between internal and client-servicing platforms.

The bank did not want its clients to have to prepare files that then needed to be sent to the bank and processed. Instead it created a channel of interaction and communication with the client so that data could flow seamlessly based on algorithms.

By taking advantage of data, AGTB has sped up its internal processes and is making smarter decisions. Through Microsoft’s cloud solutions, the bank now has a business built on data, enabling it to access a single view of the client and its banking operations.

More advanced and sophisticated banking

The financial services industry across MEA is often considered one of the most sophisticated and innovative in the world. Lafferty’s annual Global Bank Quality study, for example, has consistently rated South Africa’s banks among the most advanced and well-functioning, with an average quality score of 3.7/5 – far above averages in the US (2.8) and UK (3.5). South African bank Capitec has ranked number one for three years running, against criteria including strategy, customer engagement, organisational culture and technology adoption.

With the adoption of modern tools, local banks will continue to remain world-leading, innovating with the customer at the centre.

![A security team analyses key data from a visual dashboard.]](https://news.microsoft.com/wp-content/uploads/prod/sites/133/2023/04/Security-Sprint_TL_Banner-Image-519x260.jpg)